In accounting, a predetermined overhead rate is an allocation rate that applies a specific amount of manufacturing overhead to services or products. Typically, accountants estimate predetermined overhead at the beginning of each reporting period. If you have a company related to manufacturing, or you work as an accountant for such a business, it’s essential to calculate and monitor the predetermined overhead rate. This rate helps monitor expenses to produce goods or provide services while setting a reasonable price to earn profit.

Component Categories under Traditional Allocation

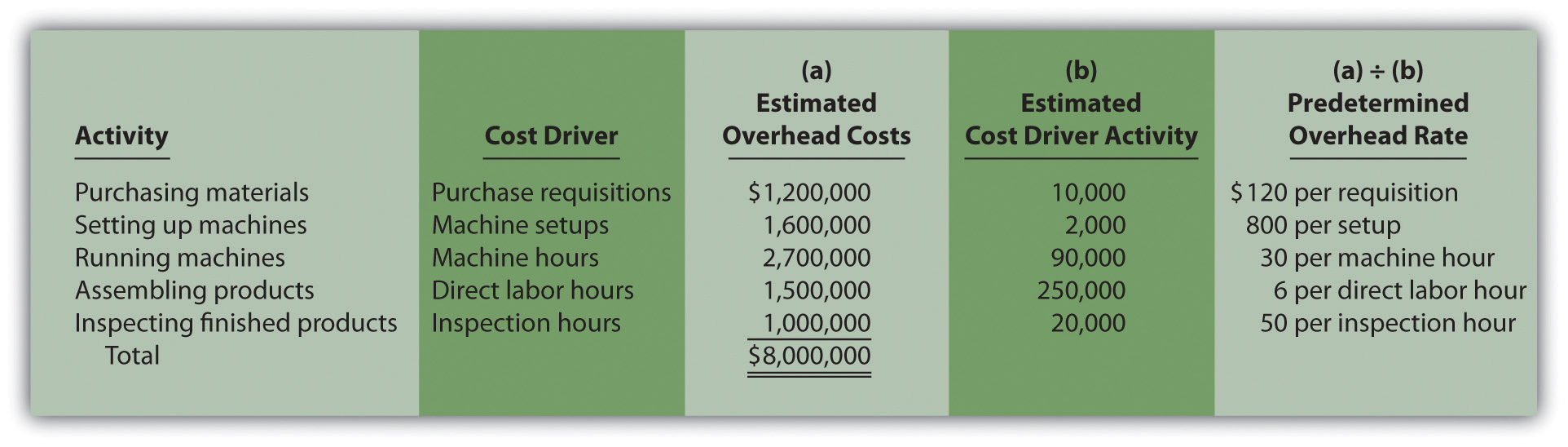

Cost accountants want to be able to estimate and allocate overhead costs like rent, utilities, and property taxes to the production processes that use these expenses indirectly. Since they can’t just arbitrarily calculate these costs, they must use a rate. However, the use of multiple predetermined overhead rates also increases the amount of required accounting labor.

- Overhead for a particular division, product, or process is commonly linked to a specific allocation base.

- The rate avoids collecting actual manufacturing overhead costs as part of the closing period.

- Different businesses have different ways of costing; some would use the single rate, others the multiple rates, while the rest may make use of activity-based costing.

- Obotu has 2+years of professional experience in the business and finance sector.

- Predetermined overhead rates help organizations in crafting comprehensive budgets that incorporate both direct and indirect costs, and in setting financial targets and performance benchmarks.

How to calculate the predetermined overhead rate: Example 3

We’ll outline the basic formulas used to calculate different types of overhead rates and provide overhead cost examples. Rather than lump overhead costs into one expense account, businesses should allocate fixed and variable overhead to departments. However, the problem with absorption/traditional costing is that we have to ignore individual absorption bases and absorb all overheads using a single level of activity. Hence, this is a compromise on the accuracy of the overall allocation process.

Formula to Calculate POHR.

The more you know about your costs, the easier it is to make informed decisions. Knowing the overhead cost per unit allows the business to set competitive pricing while still covering their indirect expenses. This $4 what are state income taxes per DLH rate would then be used to apply overhead to production in the accounting period. The difference between actual and applied overhead is later assessed to determine over- or under-application of overhead.

Common Overhead Costs to Monitor

You can calculate this rate by dividing the estimated manufacturing overhead costs for the period by the estimated number of units within the allocation base. On your current project (coded as J-17), your division has spent $2,600 on direct materials; therefore, the predetermined overhead for this project will be $4,550 ($2,600 times 175%). The overhead cost per unit from Figure 6.4 is combined with the direct material and direct labor costs as shown in Figure 6.3 to compute the total cost per unit as shown in Figure 6.5.

They represent a percentage or rate that is applied to an appropriate cost driver, such as labor hours or machine hours, to assign overhead costs to products. Now that all parts of the equation are determined let’s calculate the predetermined overhead rate. Assume that management estimates that the labor costs for the next accounting period will be $100,000 and the total overhead costs will be $150,000. This means that for every dollar of direct labor cost a production process uses, it will use $1.50 of overhead costs. The activity driver, also known as the allocation base, is the factor used to assign overhead costs to products.

Accurately calculating overhead rates is important for determining the full cost of a product and appropriately pricing goods and services. If overhead costs rise rapidly, increasing overhead rates will make this clear. Predetermined overhead is an estimated rate used by the business to absorb overheads in the product cost, and it’s calculated by dividing overheads by the budgeted level of activity. Both figures are estimated and need to be estimated at the start of the project/period. When you determine all company’s manufacturing overhead costs, add them to get the total. The predetermined overhead rate, also known as the plant-wide overhead rate, is used to estimate future manufacturing costs.

We will also explore how Sourcetable allows you to calculate this and utilize other AI-powered tools through its innovative spreadsheet assistant, which you can try at app.sourcetable.com/signup. Analyzing overhead rates by department in this manner helps identify problem areas and opportunities to improve profitability. Calculating overhead rates accurately is critical, yet often confusing, for businesses. Hence, the fish-selling businesses need to monitor the seasonal variations and adjust the cost pattern of the products.

As a result, the overhead costs that will be incurred in the actual production process will differ from this estimate. The activity base (also known as the allocation base or activity driver) in the formula for predetermined overhead rate is often direct labor costs, direct labor hours, or machine hours. The activity base can differ depending on the nature of the costs involved. That is, a number of possible allocation bases such as direct labor hours, direct labor dollars, or machine hours can be used for the denominator of the predetermined overhead rate equation. If the predetermined overhead rate is overapplied or underapplied, the potential product demand may be miscalculated as well. Overhead costs are those expenses that cannot be directly attached to a specific product, service, or process.

With $2.00 of overhead per direct hour, the Solo product is estimated to have $700,000 of overhead applied. When the $700,000 of overhead applied is divided by the estimated production of 140,000 units of the Solo product, the estimated overhead per product for the Solo product is $5.00 per unit. The computation of the overhead cost per unit for all of the products is shown in Figure 6.4. The rate is determined by dividing the fixed overhead cost by the estimated number of direct labor hours.